According to Future Market Insights (FMI), the global orthopedic power tools market is experiencing steady growth, supported by increasing orthopedic surgical volumes, advancements in surgical technology, and rising demand for precision-driven procedures. Growing prevalence of musculoskeletal disorders, an aging population, and the expansion of ambulatory surgical centers are encouraging healthcare providers to invest in advanced orthopedic power tools that improve surgical efficiency, accuracy, and patient outcomes.

Quick Stats Snapshot – Orthopedic Power Tools Market

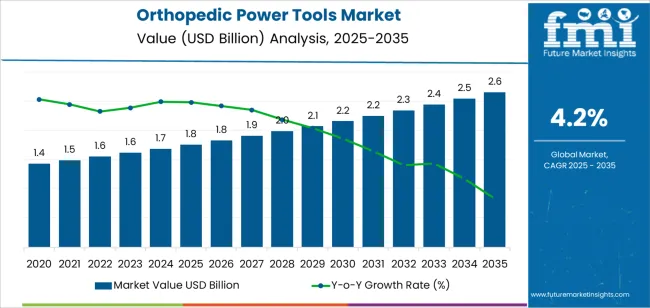

• 2025 Market Size: USD 1.8 billion

• 2035 Forecast: USD 2.6 billion

• CAGR (2025–2035): 4.2%

• Leading Product Segment: Large Bone Orthopedic Power Tools (29.0% share)

• Leading Modality Segment: Reusable Power Orthopedic Tools (70.7% share)

• Leading Technology Segment: Battery-powered Systems (39.8% share)

• Incremental Opportunity (2025–2035): USD 0.8 billion

• Key Growth Regions: North America, Asia-Pacific, Europe

• Leading Companies: Zimmer Biomet, Stryker, DePuy Synthes, Medtronic, ConMed Corporation, B. Braun Melsungen AG, De Soutter Medical

Request for a Sample: https://www.futuremarketinsights.com/reports/sample/rep-gb-646

Market Size and Outlook

The global orthopedic power tools market is projected to reach USD 2.6 billion by 2035, growing from approximately USD 1.8 billion in 2025. Market growth is being driven by increasing demand for orthopedic surgeries, including joint replacement, trauma fixation, spinal procedures, and sports injury treatments.

Orthopedic power tools have become essential components of modern surgical practice, enabling surgeons to perform procedures with greater precision, speed, and control while reducing operating times and improving procedural outcomes.

Growth Drivers: Rising Surgical Volumes and Technology Advancements

The market is primarily supported by increasing orthopedic disease burden and continuous innovation in surgical technologies.

• Growing Incidence of Musculoskeletal Disorders: Rising prevalence of osteoarthritis, osteoporosis, fractures, and sports-related injuries increasing procedure volumes

• Aging Global Population: Expanding geriatric population driving demand for joint replacement and reconstructive surgeries

• Technological Advancements: Improvements in motor performance, ergonomic designs, and modular tool configurations enhancing surgical efficiency

• Robotic-Assisted Orthopedic Procedures: Growing integration of orthopedic power tools with robotic surgery platforms improving procedural precision

• Expansion of Ambulatory Surgical Centers: Increasing shift toward outpatient orthopedic procedures supporting demand for portable and efficient power systems

These factors continue to strengthen long-term demand for advanced orthopedic surgical equipment worldwide.

Access Full Report: https://www.futuremarketinsights.com/reports/orthopedic-power-tools-market

Key Challenges: High Equipment Costs and Regulatory Requirements

Despite favorable growth prospects, manufacturers and healthcare providers face several challenges:

• High Capital Investment: Advanced orthopedic power systems requiring significant upfront procurement costs

• Regulatory Compliance Requirements: Stringent medical device approval and quality standards impacting product development timelines

• Equipment Maintenance Expenses: Ongoing servicing and sterilization requirements increasing operational costs

• Competitive Pricing Pressures: Healthcare providers seeking cost-effective solutions while maintaining clinical performance

Manufacturers focusing on product innovation, workflow optimization, and cost-efficiency are expected to maintain competitive advantages.

Opportunities: Battery Technology, Smart Surgery, and Digital Integration

Several emerging opportunities are reshaping the orthopedic power tools landscape:

• Battery-Powered Innovation: Improved lithium-ion batteries delivering longer runtime and greater mobility in operating rooms

• Smart Surgical Platforms: Integration with robotic and navigation-assisted surgical systems enhancing procedural accuracy

• Wireless Connectivity Solutions: Bluetooth and Wi-Fi-enabled tools improving surgical workflow and device communication

• 3D Printing Adoption: Increasing use of customized implants and surgical guides supporting precision tool requirements

These developments are expected to create new growth avenues for orthopedic device manufacturers globally.

Segmentation Insights: Large Bone Tools and Reusable Systems Lead Demand

• Product Segment: Large Bone Orthopedic Power Tools dominate with 29.0% share due to widespread use in joint replacement and trauma surgeries

• Modality Segment: Reusable Power Orthopedic Tools account for 70.7% share owing to long-term cost savings and sustainability benefits

• Technology Segment: Battery-powered Systems lead with 39.8% share supported by portability and workflow flexibility

• End User Segment: Hospitals remain the primary purchasing channel due to high surgical procedure volumes

• Emerging Trend: Increased adoption of cordless systems reducing operating room complexity and contamination risks

Regional Analysis: North America and Asia-Pacific Drive Market Expansion

North America continues to lead the orthopedic power tools market due to advanced healthcare infrastructure, high procedure volumes, and rapid adoption of innovative surgical technologies.

• United States: Strong demand driven by aging demographics, high orthopedic surgery volumes, and robotic-assisted surgical adoption

• Europe: Growing focus on efficient and value-based orthopedic care supporting equipment upgrades

• China: Expanding healthcare infrastructure and increasing healthcare spending accelerating market growth

• Asia-Pacific: Rising orthopedic disease burden and improved access to surgical care creating significant opportunities

• United Kingdom: Emphasis on surgical efficiency and healthcare cost optimization supporting adoption of advanced orthopedic technologies

Competitive Landscape: Robotics Integration and Product Innovation Shape Competition

The orthopedic power tools market remains highly competitive, with manufacturers focusing on innovation, ergonomics, and integration with advanced surgical systems.

Leading companies focus on:

• Developing battery-powered and cordless orthopedic power tools

• Expanding robotic-assisted surgery compatibility

• Improving ergonomics and surgeon comfort

• Enhancing power-to-weight ratios and device durability

• Strengthening partnerships with hospitals and ambulatory surgical centers

Competitive advantage increasingly depends on technological innovation, procedural efficiency, reliability, and integration with digital surgical ecosystems.

Strategic Implications for Decision-Makers

The orthopedic power tools market presents attractive long-term opportunities supported by increasing orthopedic procedure volumes and technological innovation.

• Hospitals should prioritize advanced orthopedic systems that improve efficiency and surgical precision

• Ambulatory surgical centers can benefit from lightweight and battery-powered tools that enhance mobility and workflow

• Investors may capitalize on growing demand for robotic-assisted orthopedic procedures and surgical automation technologies

• Manufacturers investing in battery innovation, connectivity features, and smart surgical platforms are expected to strengthen market positioning

As orthopedic procedures continue to rise globally and healthcare providers focus on improving patient outcomes, orthopedic power tools are expected to remain indispensable components of modern surgical practice.

FAQs

What is the future size of the market?

The orthopedic power tools market is projected to reach USD 2.6 billion by 2035.

What is driving market growth?

Growth is driven by increasing orthopedic surgeries, rising musculoskeletal disorders, technological advancements, and growing adoption of robotic-assisted procedures.

Which product segment dominates the market?

Large Bone Orthopedic Power Tools lead the market with a 29.0% share in 2025.

Which modality segment holds the largest market share?

Reusable Power Orthopedic Tools dominate with a 70.7% share due to their long-term cost-effectiveness and sustainability benefits.

Which technology segment leads the market?

Battery-powered Systems account for the largest technology share at 39.8% in 2025.

Which companies are leading the market?

Key players include Zimmer Biomet, Stryker, DePuy Synthes, Medtronic, ConMed Corporation, B. Braun Melsungen AG, De Soutter Medical, and Johnson & Johnson.

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

For Press & Corporate Inquiries:

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For Web - https://www.futuremarketinsights.com/

For Web - https://www.factmr.com/