The global automotive automatic transmission market is entering a pivotal transition period as automakers balance fuel efficiency targets, electrification strategies, emissions compliance, and evolving consumer expectations around driving comfort. What was once viewed primarily as a mechanical drivetrain component is increasingly becoming a strategic technology platform tied to vehicle intelligence, hybrid integration, energy optimization, and next-generation mobility systems.

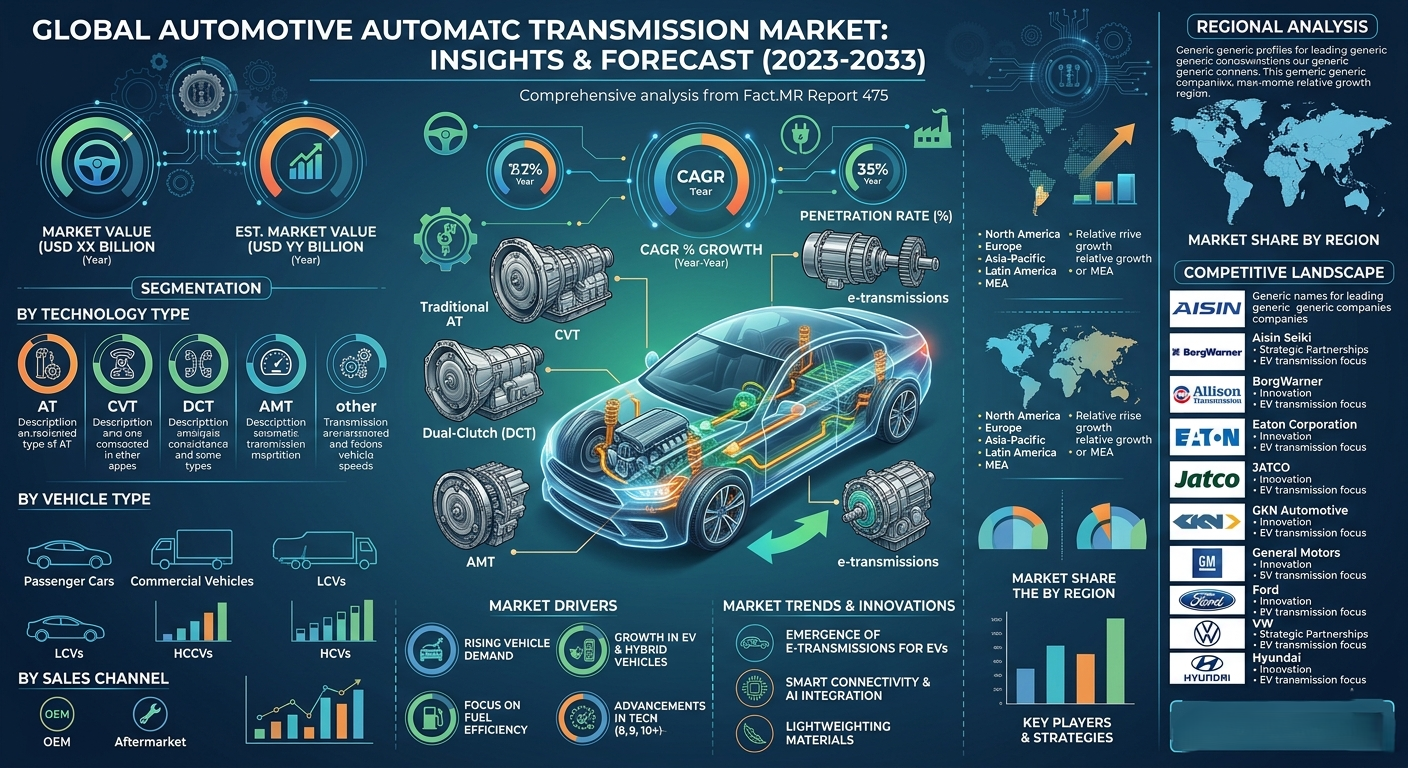

Automotive Automatic Transmission Market Size Global revenue from automotive automatic transmission systems is projected to rise from US$ 76.11 billion in 2024 to US$ 122.81 billion by 2034, expanding at a CAGR of 3.6%. While traditional automatic systems continue to dominate passenger vehicles, the next decade is expected to be shaped by the rapid adoption of dual-clutch transmissions (DCTs), continuously variable transmissions (CVTs), electrified drivetrains, and software-controlled transmission architectures.

The transformation is occurring at a time when global automotive manufacturers face mounting pressure to reduce emissions, improve energy efficiency, and support hybrid and electric vehicle platforms without compromising performance or driver experience.

Quick Stats: Automotive Automatic Transmission Market

- Market Size (2024): US$ 76.11 Billion

- Forecast Value (2034): US$ 122.81 Billion

- Forecast CAGR (2024–2034): 3.6%

- North America Market Share (2024): 35.7%

- East Asia Market Share (2024): 29.8%

- Passenger Vehicles Segment (2034): US$ 89.16 Billion

- OEM Revenue Contribution (2024): US$ 58.23 Billion

- Fastest-Growing National Market: China

- Key Technologies:

- DCT (Dual-Clutch Transmission)

- CVT (Continuously Variable Transmission)

- Hybrid Transmission Systems

Automatic Transmissions Are Becoming Central to Vehicle Efficiency Strategies

The automotive industry’s accelerating shift toward electrification and low-emission mobility is fundamentally reshaping transmission system development.

Manufacturers are increasingly focusing on lightweight transmission architectures, intelligent gear systems, and electrified drivetrains to comply with tightening environmental regulations across North America, Europe, and Asia Pacific.

Transmission systems are no longer designed solely around mechanical performance. Instead, they are now expected to contribute directly to:

- Fuel economy optimization

- CO2 emissions reduction

- Energy recovery efficiency

- Hybrid powertrain integration

- Smooth driving dynamics

- Advanced driver assistance compatibility

This evolution is particularly important as governments worldwide continue tightening fleet emission standards and promoting low-carbon transportation ecosystems.

Automotive suppliers are responding by incorporating lightweight materials such as aluminum, magnesium, and advanced steel composites into transmission production. Additive manufacturing and precision engineering technologies are also enabling more compact and efficient transmission structures without sacrificing durability.

Consumer Preference Is Rapidly Moving Away From Manual Systems

Consumer driving behavior has changed significantly over the past decade, particularly in urban markets where traffic congestion and convenience increasingly influence vehicle purchasing decisions.

Automatic transmissions are now widely associated with:

- Smoother driving experiences

- Better fuel efficiency in modern systems

- Reduced driver fatigue

- Enhanced integration with hybrid vehicles

- Improved performance optimization

In the United States, automatic transmissions already dominate the market. According to industry estimates, automatic systems account for the overwhelming majority of passenger vehicle usage, reflecting long-term consumer preference shifts.

Emerging economies are now following similar adoption patterns, especially in urban middle-class passenger vehicle segments.

The growing popularity of electric vehicles is accelerating this transition further. Electrified vehicles inherently favor automated power delivery systems, reinforcing demand for advanced transmission technologies that can optimize battery performance and torque management.

Hybrid and Electric Vehicle Expansion Is Reshaping Transmission Innovation

One of the most significant structural growth drivers in the market is the global rise of hybrid and electric mobility.

While fully electric vehicles often use simplified drivetrain architectures, hybrid systems still rely heavily on advanced transmission technologies to manage energy distribution between combustion engines and electric motors.

This has created growing demand for:

- Electrified dual-clutch systems

- Integrated e-drive transmissions

- Hybrid-ready CVT platforms

- Smart transmission control software

- Energy-efficient torque management systems

Automakers increasingly view transmission systems as critical enablers of hybrid vehicle efficiency rather than standalone drivetrain components.

The long-term market opportunity therefore extends beyond conventional automatic gearboxes into intelligent powertrain integration systems.

Lightweight Engineering Is Emerging as a Competitive Imperative

Weight reduction has become one of the automotive sector’s most important engineering priorities.

Regulators continue pushing for lower emissions and higher efficiency standards, forcing manufacturers to optimize every major vehicle component for weight savings.

Transmission systems have consequently become a major focus area for lightweight innovation.

Manufacturers are increasingly deploying:

- Aluminum housing systems

- Magnesium components

- High-strength lightweight alloys

- Compact transmission architectures

- 3D-printed structural elements

These innovations improve not only emissions performance but also vehicle acceleration, braking responsiveness, and handling characteristics.

For automakers, lighter transmission systems can contribute meaningfully to overall fleet efficiency targets without requiring radical platform redesigns.

Cost and Complexity Continue to Challenge Wider Adoption

Despite strong growth momentum, the market continues to face several structural constraints.

Advanced transmission technologies such as DCTs and CVTs remain significantly more complex and expensive than conventional systems. Maintenance and repair costs are also higher because these systems require specialized expertise and advanced diagnostics.

This presents a challenge in cost-sensitive vehicle segments, particularly in developing markets where affordability remains a critical purchasing factor.

Manufacturers must therefore balance three competing priorities:

- Fuel efficiency improvement

- Advanced performance capabilities

- Cost optimization for mass-market adoption

The industry’s ability to reduce production complexity while maintaining technological sophistication will play a major role in determining future adoption rates.

Passenger Vehicles Continue to Drive Market Revenue

Passenger vehicles remain the dominant application segment and are expected to generate US$ 89.16 billion in market value by 2034.

Several trends continue supporting segment leadership:

- Rising urban vehicle ownership

- Consumer preference for comfort-focused driving

- Increased adoption of hybrid passenger cars

- Growth in premium vehicle sales

- Expansion of electric mobility ecosystems

While commercial vehicle applications are also growing, passenger vehicles continue representing the primary volume driver for transmission manufacturers globally.

The segment’s expansion is especially pronounced in Asia Pacific, where middle-income vehicle ownership continues rising rapidly.

OEMs Maintain Strategic Control Over Market Revenue

Original equipment manufacturers (OEMs) are projected to account for the majority of market revenue throughout the forecast period.

OEM dominance reflects the growing technical complexity of transmission systems and the importance of integrated vehicle-platform engineering.

Automakers increasingly prefer tightly integrated transmission ecosystems that ensure:

- Software compatibility

- Performance consistency

- Regulatory compliance

- Warranty protection

- Energy optimization

OEMs are also leveraging advanced manufacturing technologies such as 3D printing and digital supply chain systems to improve production flexibility and reduce operational costs.

Meanwhile, aftermarket suppliers continue serving replacement and maintenance demand, particularly in aging vehicle fleets.

North America Leads Current Revenue Generation

North America is projected to account for 35.7% of global market share in 2024, maintaining its leadership position due to high automatic transmission adoption rates and strong consumer preference for comfort-oriented driving systems.

The United States alone is expected to reach US$ 29.18 billion by 2034, growing at a CAGR of 5.5%.

Several structural factors support US market expansion:

- High penetration of automatic vehicles

- Rising hybrid and EV adoption

- Consumer preference for premium driving experiences

- Demand for fuel-efficient SUVs and crossovers

- Strong OEM manufacturing presence

The region also benefits from robust automotive R&D investment and advanced supplier ecosystems focused on drivetrain innovation.

China Is Emerging as the Industry’s Most Strategic Growth Market

China is forecast to grow at a CAGR of 6.2% through 2034, making it one of the fastest-expanding automotive automatic transmission markets globally.

The country’s automotive sector continues evolving rapidly due to:

- Expanding passenger vehicle ownership

- Strong domestic EV production

- Urban mobility demand

- Government-backed electrification policies

- Rising middle-class consumer expectations

Automatic transmissions are gaining significant traction in low- and mid-range passenger vehicle categories, where manual systems historically dominated.

China’s position as both a manufacturing hub and consumption market gives it outsized influence over future transmission technology development and supply chain dynamics.

East Asia Is Becoming a Transmission Innovation Hub

East Asia’s growing market share reflects the region’s broader role in automotive electrification and advanced manufacturing.

Countries such as China, South Korea, and Japan are increasingly investing in:

- Hybrid transmission systems

- Electrified drivetrains

- Smart mobility integration

- Lightweight automotive engineering

- Precision manufacturing technologies

Regional automakers and suppliers are positioning themselves as global leaders in next-generation transmission development.

As EV and hybrid production volumes increase, East Asia is expected to remain central to drivetrain innovation throughout the next decade.

Competitive Landscape Is Shifting Toward Electrified Powertrain Leadership

The competitive environment is increasingly shaped by companies capable of integrating mechanical engineering expertise with electrification, software systems, and advanced mobility technologies.

Major industry participants include:

- Honda Motor Co., Ltd.

- Yamaha Motor Co. Ltd.

- Hyundai Motor Company

- Aisin Corporation

- ZF Friedrichshafen AG

- Magna International Inc.

- JATCO Ltd.

- BorgWarner Inc.

- Allison Transmission

- Schaeffler AG

Strategic investments increasingly focus on:

- Mild hybrid transmission systems

- Electrified drivetrain platforms

- Smart energy management

- CO2 reduction technologies

- Compact high-efficiency architectures

Recent developments indicate that competitive differentiation is moving beyond mechanical reliability toward integrated electrification capability.

Strategic Implications for Industry Stakeholders

For automakers, transmission technologies are becoming critical to broader mobility platform strategies rather than isolated component categories.

OEMs that successfully integrate intelligent transmission systems with electrified drivetrains may gain meaningful advantages in:

- Fleet emissions compliance

- Vehicle energy efficiency

- Consumer driving experience

- Platform scalability

- Hybrid vehicle competitiveness

For suppliers, future competitiveness will increasingly depend on software integration capabilities and electrified powertrain partnerships.

For investors, the market presents a relatively stable long-term industrial growth opportunity linked closely to global electrification trends and regulatory transitions.

Future Outlook: Transmission Systems Become Software-Defined Mobility Components

The next decade is expected to redefine the role of automatic transmissions within the automotive ecosystem.

Rather than functioning solely as mechanical gear-shifting systems, transmissions are increasingly evolving into intelligent, software-integrated mobility components optimized for hybridization, automation, and energy management.

Growth will likely remain strongest in:

- Hybrid vehicle platforms

- Fuel-efficient passenger vehicles

- Electrified urban mobility systems

- Lightweight automotive architectures

- Smart drivetrain ecosystems

Manufacturers capable of balancing efficiency, affordability, electrification readiness, and software integration are expected to shape the next phase of industry leadership.

Executive-Level Takeaways

- The global automotive automatic transmission market is projected to reach US$ 122.81 billion by 2034.

- Electrification and hybrid vehicle expansion are fundamentally reshaping transmission system design.

- Lightweight engineering and advanced materials are becoming strategic priorities for automakers.

- Consumer preference continues shifting decisively toward automatic systems globally.

- China and East Asia are emerging as critical innovation and production centers.

- OEMs remain dominant due to the increasing complexity of integrated drivetrain architectures.

- DCT and CVT technologies are gaining momentum as efficiency-focused alternatives.

- Future competitive advantage will increasingly depend on electrification integration, software capability, and energy optimization performance.

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com