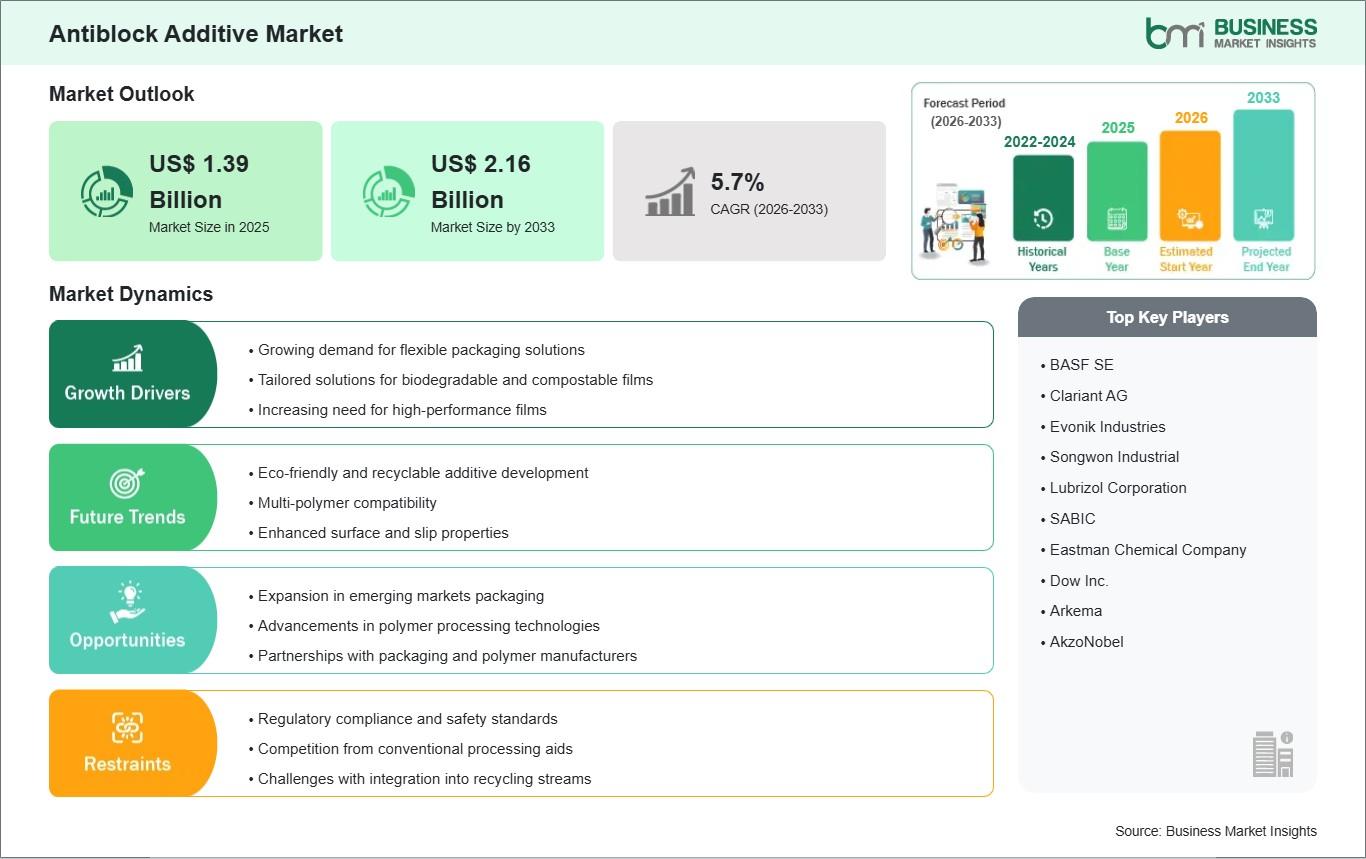

According to the Business Market Insights The Global Antiblock Additive Market is witnessing steady growth driven by the increasing demand for high-performance polymer films and flexible packaging solutions. Antiblock additives play a crucial role in reducing film-to-film adhesion, enhancing processing efficiency, and improving the overall quality of plastic films used across industries such as food packaging, pharmaceuticals, and agriculture. As per insights from Business Market Insights, the market was valued at US$ 1.39 billion in 2025 and is projected to reach US$ 2.16 billion by 2033, expanding at a CAGR of 5.7% during 2026–2033.

A key factor supporting this growth is the rapid expansion of flexible packaging applications, where antiblock additives ensure smooth film handling and prevent sticking issues. Additionally, technological advancements in polymer processing and rising sustainability concerns are further shaping the market landscape. The growing adoption of eco-friendly packaging materials is encouraging manufacturers to develop innovative antiblock solutions that align with regulatory standards and environmental goals.

Download Sample PDF Copy: https://www.businessmarketinsights.com/sample/BMIPUB00033763

Market Report Segmentation Analysis

A detailed segmentation analysis provides a comprehensive understanding of the antiblock additive market by categorizing it into product type, polymer type, application, and geography. This segmentation helps stakeholders identify high-growth areas and strategic investment opportunities.

By Product Type

The market is segmented into organic and inorganic antiblock additives. Among these, the inorganic segment dominated the market in 2025, primarily due to its superior efficiency in reducing film blocking and improving processing performance.

Inorganic additives such as silica, talc, and calcium carbonate are widely preferred because they create micro-rough surfaces that prevent adhesion between film layers. Their cost-effectiveness and high thermal stability make them suitable for large-scale industrial applications. On the other hand, organic additives, including fatty amides, are gaining traction due to their compatibility with specific polymers and enhanced slip properties.

By Polymer Type

Based on polymer type, the market is categorized into LLDPE, LDPE, HDPE, BOPP, PVC, and others. The LLDPE (Linear Low-Density Polyethylene) segment held the largest market share in 2025, driven by its extensive use in flexible packaging films.

LLDPE-based films are widely utilized due to their excellent tensile strength, flexibility, and puncture resistance. Similarly, LDPE and HDPE are also commonly used in packaging and industrial films. BOPP films, known for their clarity and strength, are increasingly being adopted in food packaging, further boosting the demand for antiblock additives.

By Application

The antiblock additive market is segmented into packaging and non-packaging applications. The packaging segment dominated the market in 2025, owing to the rising demand for packaged food, beverages, and consumer goods.

Packaging applications account for the majority of demand as antiblock additives enhance film clarity, machinability, and durability. In contrast, non-packaging applications include agriculture, medical, and industrial uses, where these additives improve product performance and handling efficiency.

By Geography

Geographically, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South & Central America. North America held the largest share in 2025 due to advanced packaging technologies and strict regulatory frameworks.

However, Asia-Pacific is expected to witness the fastest growth, driven by rapid industrialization, population growth, and increasing demand for packaged goods in countries like China and India. The expansion of e-commerce and retail sectors in emerging economies is further accelerating the adoption of flexible packaging, thereby boosting the demand for antiblock additives.

Competitive Landscape and Key Players

The global antiblock additive market is highly competitive, with several leading companies focusing on product innovation, mergers, and strategic collaborations to strengthen their market position. Key players operating in the market include:

- BASF SE

- Clariant AG

- Evonik Industries

- Songwon Industrial

- Lubrizol Corporation

- SABIC

- Eastman Chemical Company

- Dow Inc.

- Arkema

- AkzoNobel

These companies are investing heavily in research and development to introduce advanced antiblock formulations that offer better performance, sustainability, and compliance with regulatory standards.

Trending Keywords –

Aluminium Caps & Closures Market - Outlook (2022-2033)

Aluminium Composite Panels Market - Outlook (2022-2033)

Aluminum Rolled Products Market - Outlook (2022-2033)

Market Outlook and Opportunities

The antiblock additive market is poised for significant growth through 2033, driven by increasing demand for high-quality packaging materials and advancements in polymer technology. The shift toward sustainable packaging solutions presents lucrative opportunities for market players to develop biodegradable and recyclable antiblock additives.

Furthermore, the expansion of industries such as food processing, pharmaceuticals, and agriculture is expected to create new growth avenues. As manufacturers continue to prioritize efficiency and product quality, the adoption of advanced antiblock additives will remain a key trend shaping the market.

About Us

Business Market Insights is a leading market research and consulting firm dedicated to providing actionable insights and comprehensive industry analysis. The company specializes in delivering in-depth reports across various industries, helping clients make informed business decisions and identify growth opportunities in dynamic markets.

Contact Us

Business Market Insights

Email: sales@businessmarketinsights.com

Website: https://www.businessmarketinsights.com